Sustainability Governance

- Sustainability Governance is the system that manages the environmental and social interactions of entities that results in the entity’s sustainability performance.

- Sustainability Governance is the system through which entities are managed through their internal regulations, and society evaluates them from the point of view of sustainability.

- Sustainability Governance is managed from the implementation of policies, strategies, processes, decisions, and behaviors, which determine the entity’s performance in the areas of sustainability.

- The benefits of Sustainability Governance are measured in the better economic performance of the entity thanks to its better relationships with the social and environmental performance perceived by the actors of the economic system. A Bain study shows that 90% of companies think they have to change their business model to adapt and compete from sustainability.

- Triple Sustainability helps entities to develop, improve and manage their systems to deliver the best outcomes.

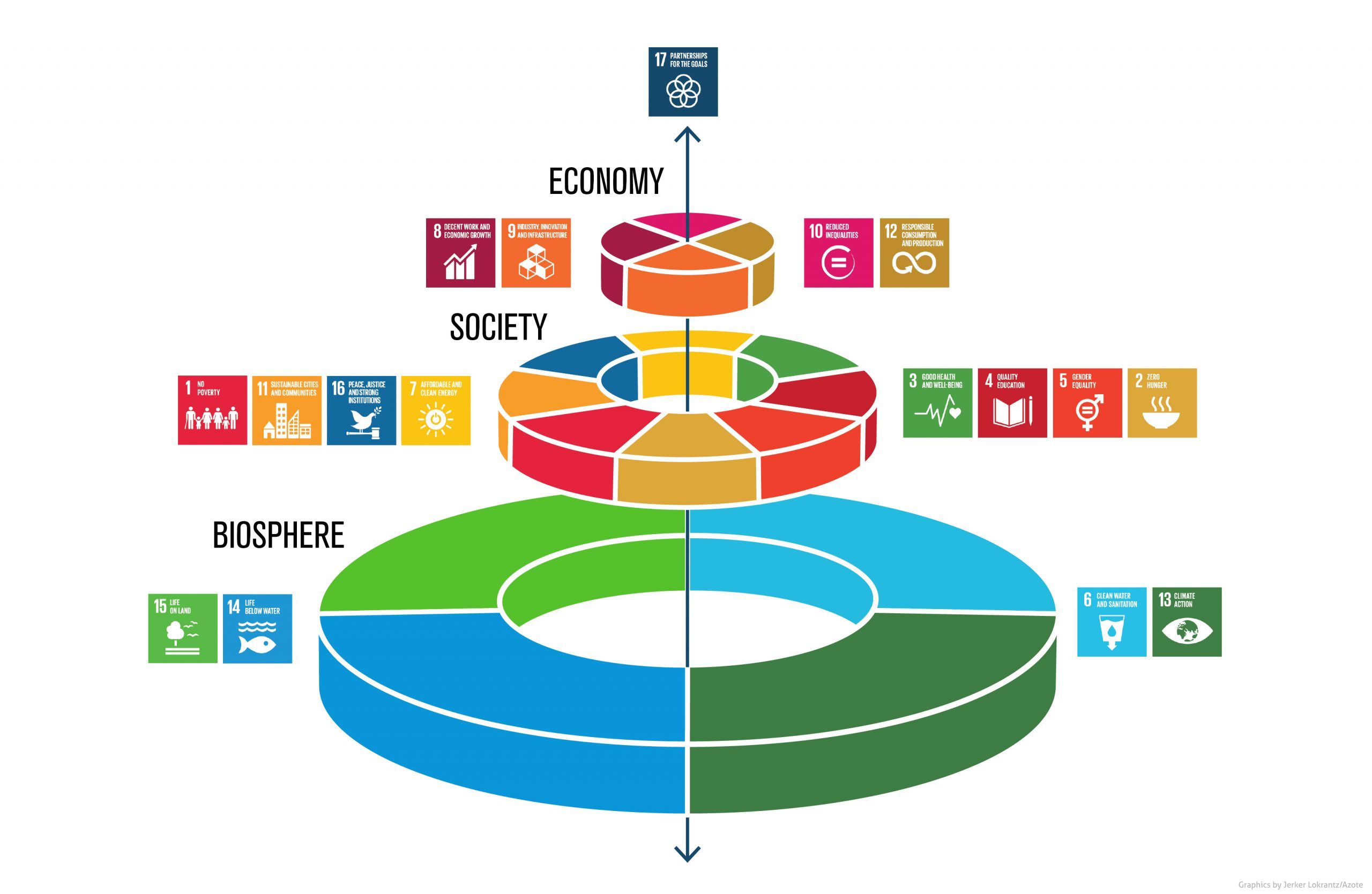

What is Sustainability?

Conditions for Sustainable Economy

- Generates more Revenue than Operational Costs including:

- Full Social Costs.

- Full Environmental Costs.

- Granted Social License.

Conditions for Sustainable Society

- Social System functioning at an acceptable level of Social Well-being.

- Wealth generated covers the costs of the Social Well-being.

Conditions for Sustainable Environment

- Renewable resources harvest rate is lower or equal to production rate.

- Non-renewable resources are recycled-reused.

- Pollution rate is lower or equal to natural treatment rate without harm.

- Biodiversity indices are stable.

What is Sustanibility Governance

Sustainability Governance

Sustainability Governance (SG) is the system by which entities are 1) managed through their internal regulations and 2) held accountable for their actions from the sustainability standpoint.

- S.G. Sets the System:

- Policies and Goals.

- Identification of Risks and Opportunities.

- Organizational Structure.

- Management Plans.

- Stakeholder Engagement and Communication System.

- Monitoring.

- Reporting.

- SG implements the system through the behaviors of the entity members at all levels.

Objectives for Sustainability Governance

Objectives for Sustainability Governance

- Enhance Performance:

- Achieve Endless Profitability.

- Hold Indefinitely a Social License to Operate.

- Operate Indefinitely within the boundaries of Net Zero Environmental Impact.

- Involve all Stakeholders in the creation of value for the company and for themselves.

- Increase and Maintain the portion of company market value based on Intangibles.

Stakeholders in Sustainability Governance

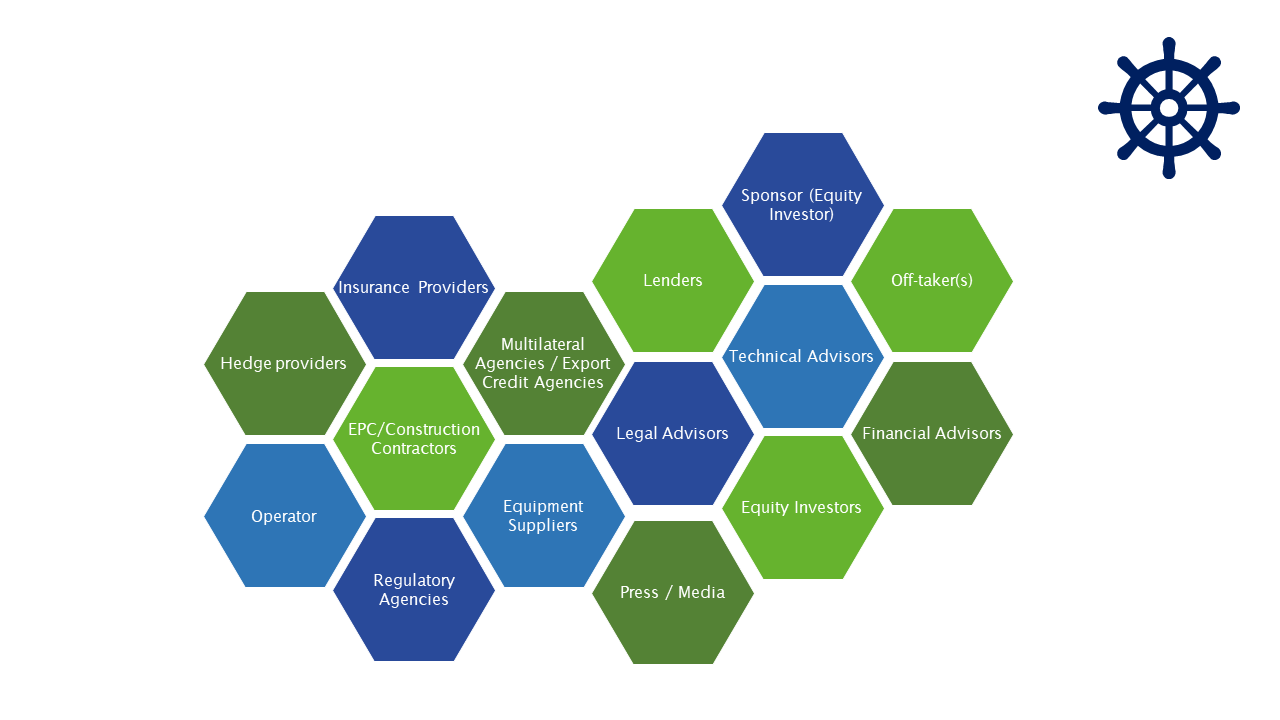

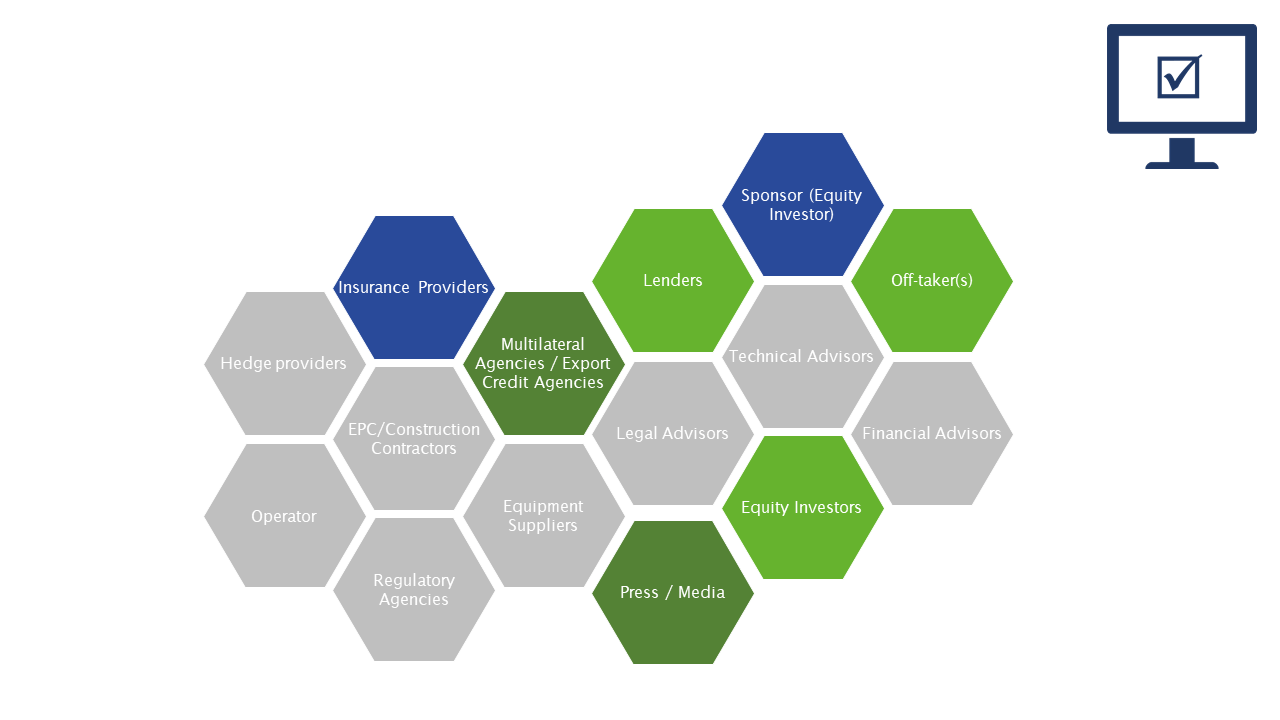

Project Level Stakeholders for Sustainability Governance

- Project Sponsor who invest in equity.

- Equity Investors.

- Off-Takers who receive the product.

- Lenders who lend the funds.

- Multilateral Agencies and Export Credit Agencies who also lend funds.

- Project Finance Facilitators:

- Legal Advisors.

- Technical Advisors.

- Financial Advisors.

- Regulatory Agencies who grant the permits and licenses.

- EPC or Construction Contractors who may engineer, procure and construct.

- Equipment Suppliers.

- Insurance Providers.

- Hedge Providers.

- Operator who will operate the facility once constructed.

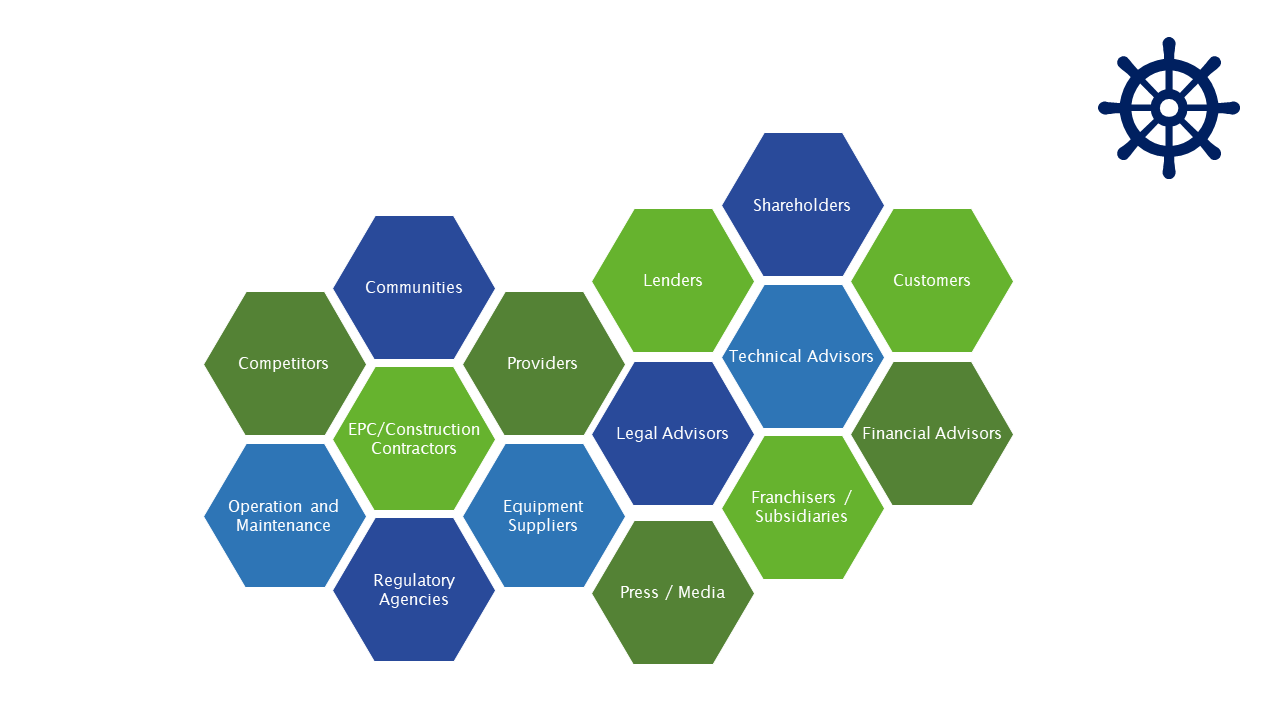

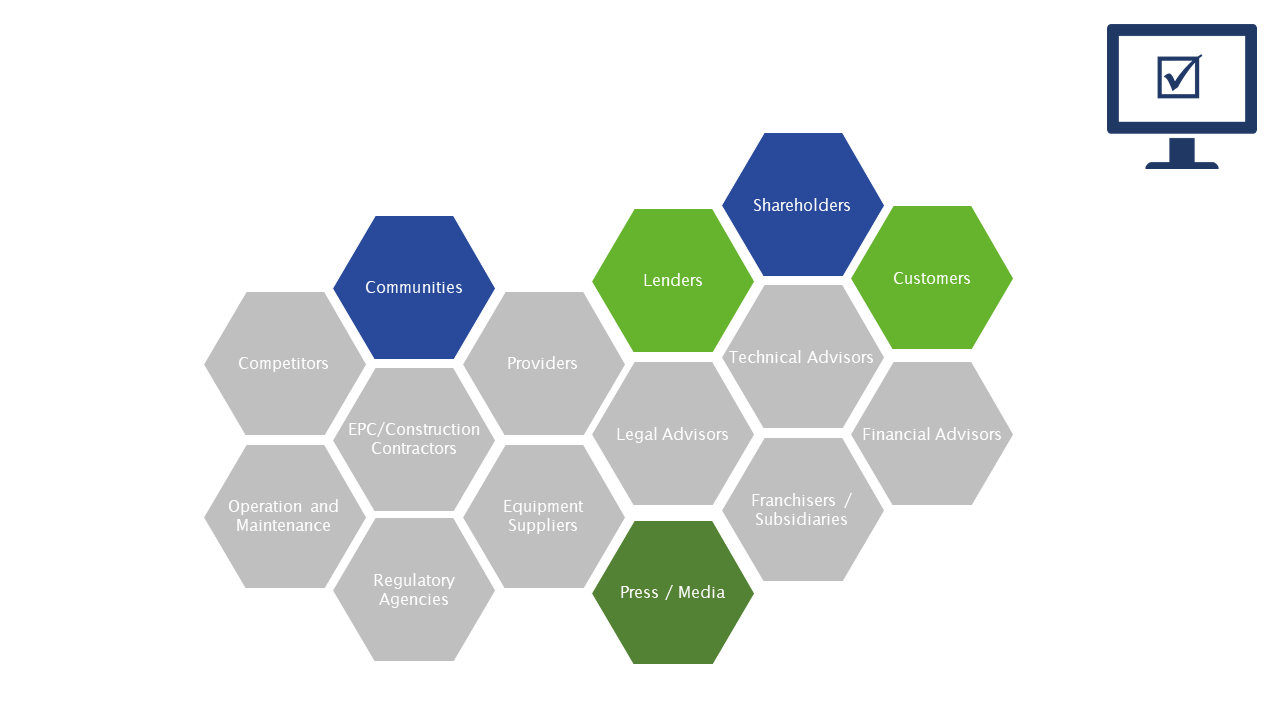

Company Level Stakeholders for Sustainability Governance

- Shareholders.

- Customers.

- Communities.

- Franchisers / Subsidiaries.

- Lenders .

- Company Advisors:

- Legal Advisors.

- Technical Advisors.

- Financial Advisors.

- Providers.

- Press / Media.

- Regulatory Agencies who grant the permits and licenses.

- Equipment Suppliers.

- EPC or Construction Contractors who may engineer, procure and construct.

- Competitors.

- Operation and Maintenance.

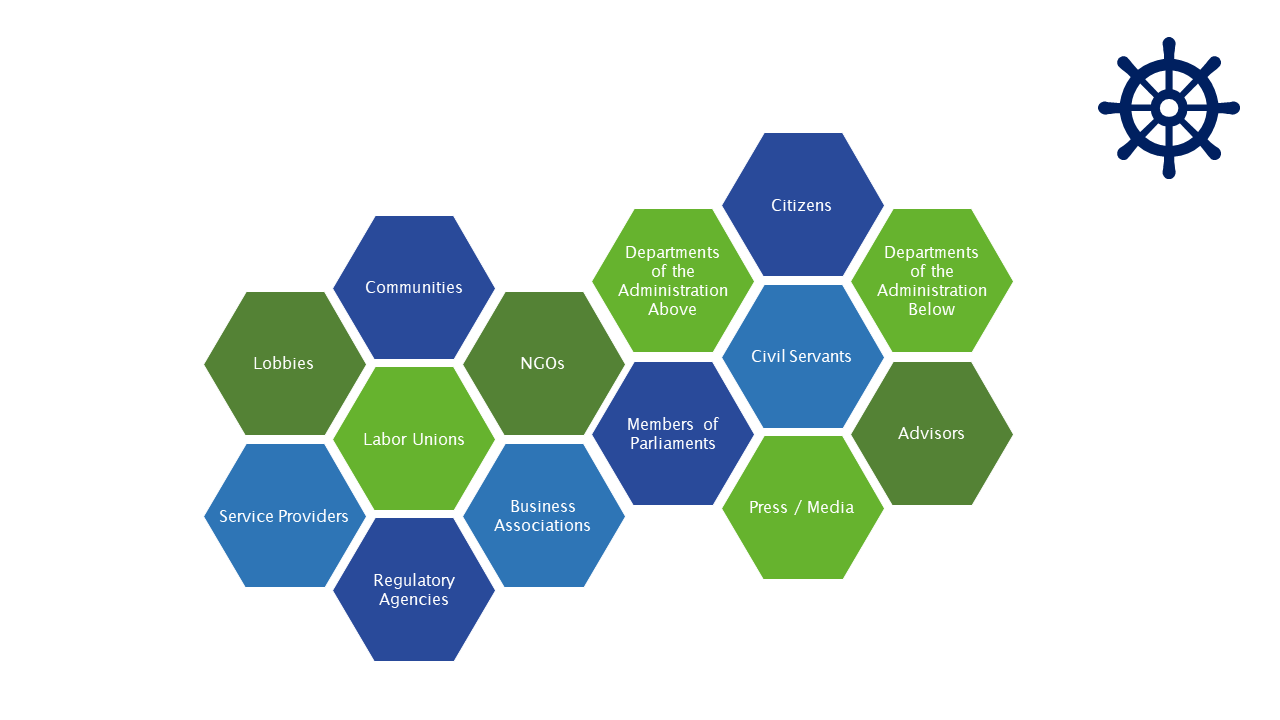

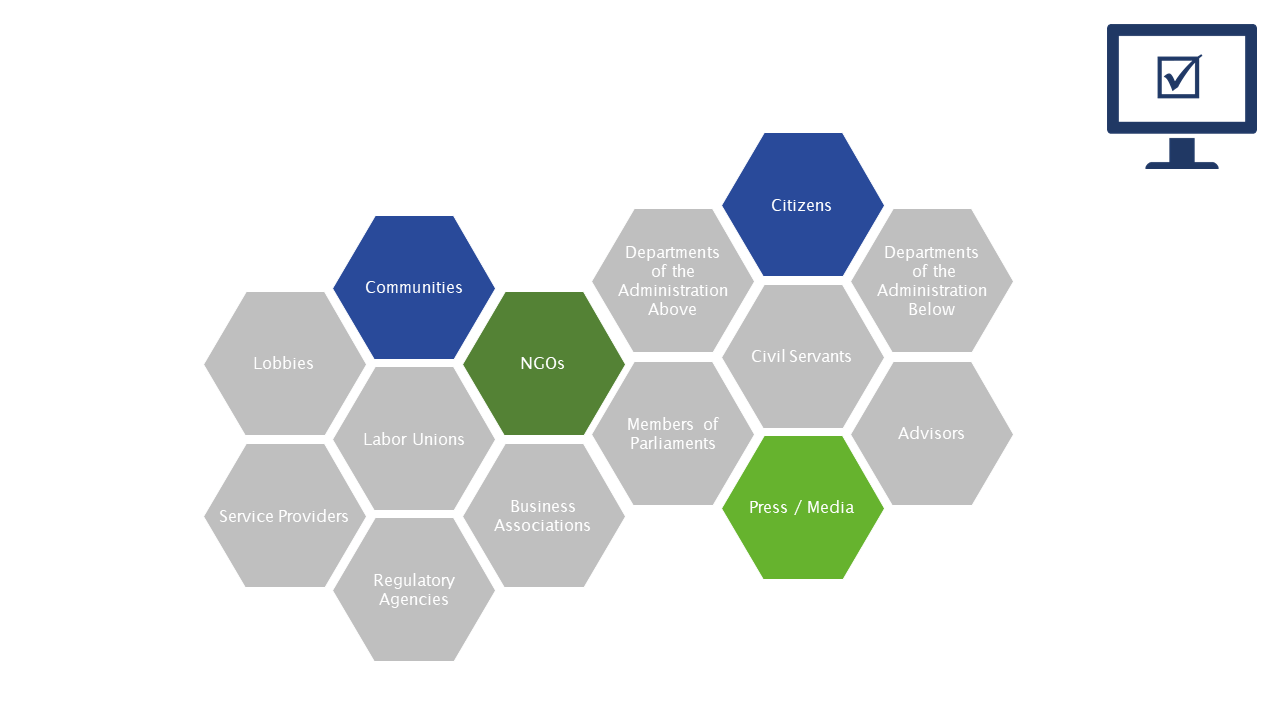

Governmental Organization Stakeholders for Sustainability Governance

- Citizens.

- Press / Media.

- Civil Servants.

- Communities.

- Departments of the Administration Below.

- Departments of the Administration Above.

- Members of Parliaments.

- Advisors.

- Non-Governmental Organizations (NGOs).

- Business Associations.

- Lobbies.

- Labor Unions.

- Regulatory Agencies.

- Service Providers.

Risks for not implementing Sustainability Governance

Project Level Risks

- Worst lending terms or even no loan financially feasible.

- A borrower is unable to repay a loan due to Environmental & Social risks.

- Non Technical disruptions causing delays and increased implementation costs.

- Reduced benefits due to unexpected Environmental & Social costs.

Company Level Risks

- Worst lending terms or even no loan financially feasible.

- Legal complications, fees, and/or fines for rectifying social and environmental damage.

- Reputational issues may reduce company value.

Governmental Organization Risks

- Citizens unsatisfied with policies and performance.

- Legal complications, fees, and/or fines for rectifying social and environmental damage.

- Reputational issues may force the governing party to exit.

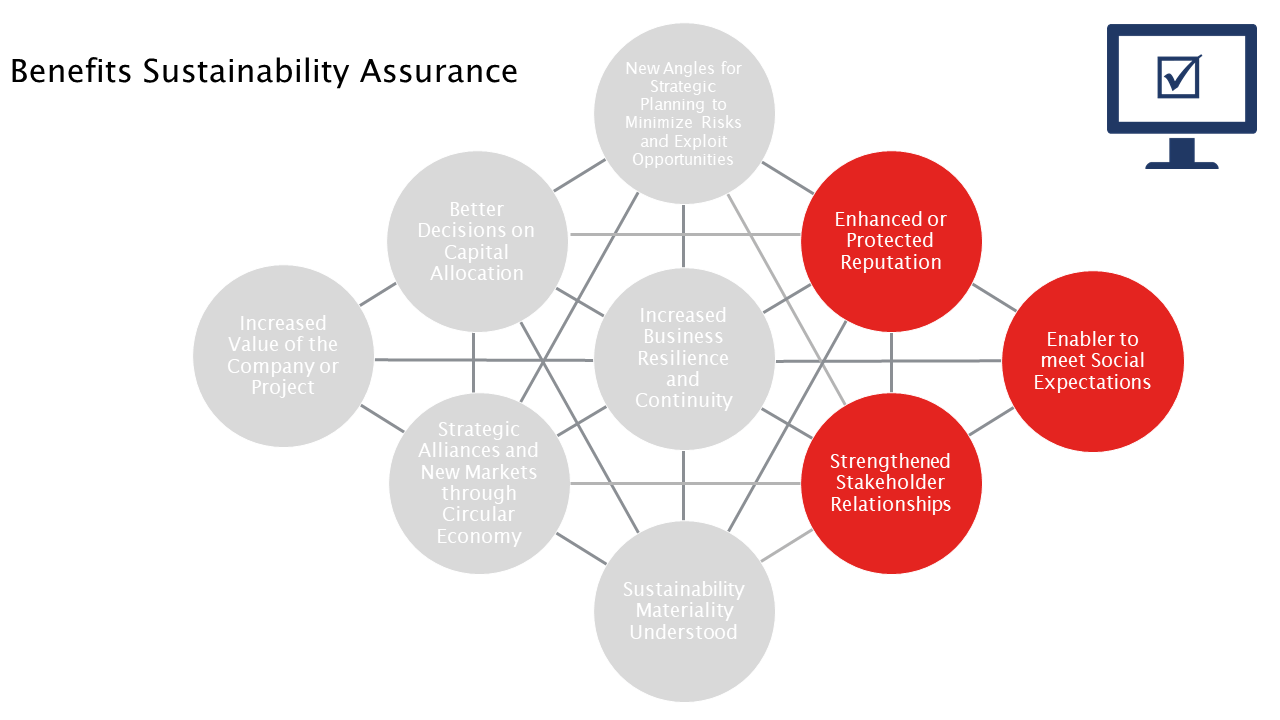

Benefits of Sustainability Governance

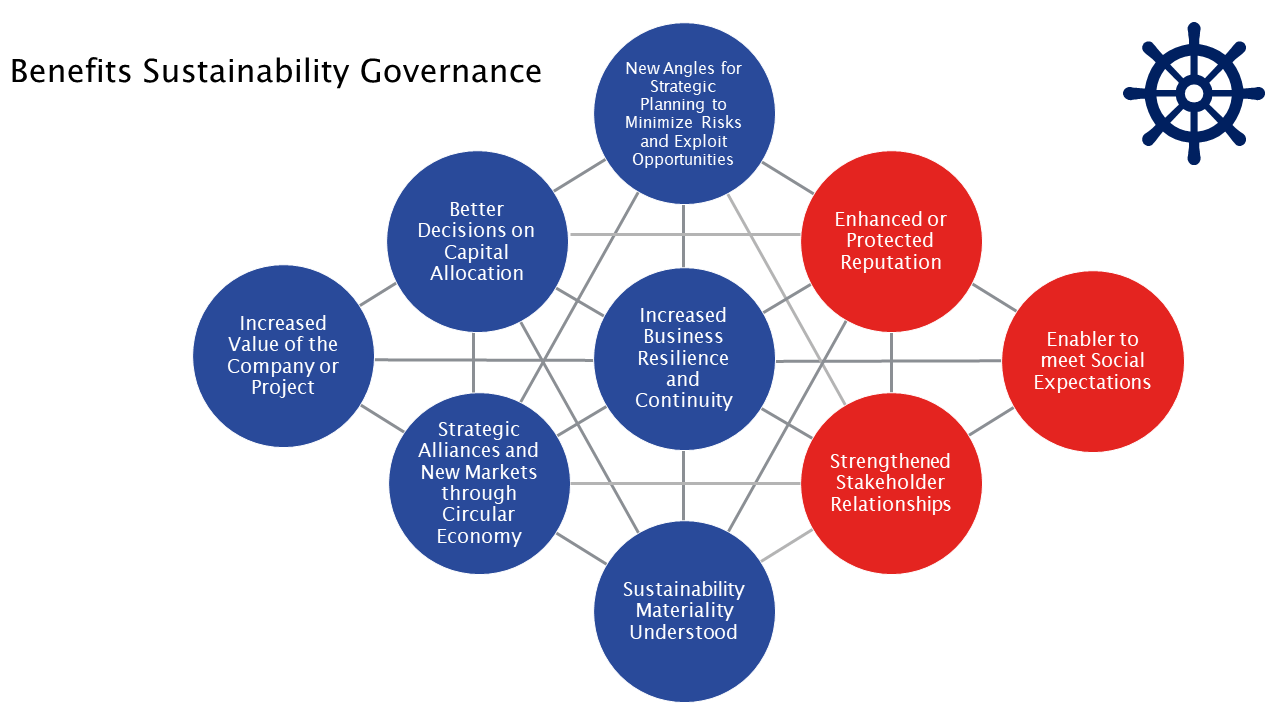

Top Benefits of Sustainability Governance

- Increased Value of the Project, Company or Entity.

- Better Decisions on Capital Allocation.

- New Angles for Strategic Planning to Minimize Risks and Exploit Opportunities.

- Strategic Alliances and New Markets through Circular Economy.

- Increased Business Resilience and Continuity.

- Sustainability Materiality Understood.

- Strengthened Stakeholders Relationships.

- Enabler to meet Social Expectations.

Sustainability Governance Implementation

Sustainability Governance Implementation

The Sustainability Governance implementation process is conceptually summarized and further explained.

Two complementary approaches should be the basis to properly develop your Sustainability Governance System:

- The Adaptive Governance (AG); and

- The Plan-Do-Check-Act (PDCA).

Adaptive Governance

The Adaptive Governance approach is an intentional approach to making decisions and adjustments in response to new information and changes in context.

The wheel presented on the right is the way USAID operationalized the concept in a very practical way.

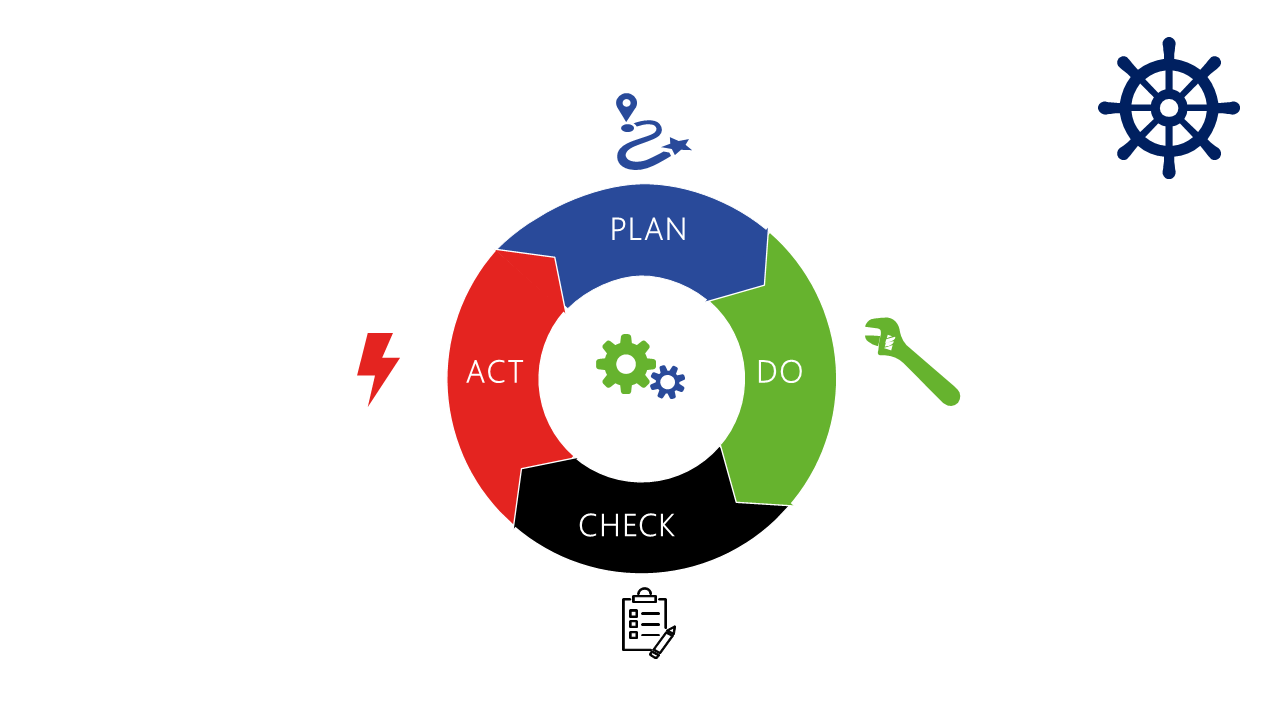

Plan-Do-Check-Act Approach

The Plan, Do, Check, Act approach provides a balance between the systems and behavioral aspects of management:

- Plan. Define and Implement the Sustainable Management System (SMS).

- Do. Follow Plans and Procedures and Register both Actions and Results.

- Check. Verify Compliance with the SMS. Review Results and Deviations and Propose Changes.

- Act. Implement Proposed Changes.

Standards for Sustainability Governance

United Nations Global Compact

2000

- Principle 1: Support and respect the protection of internationally proclaimed human rights.

- Principle 2: Not complicit in human rights abuses.

- Principle 3: Uphold the freedom of association and the effective recognition of the right to collective bargaining.

- Principle 4: Elimination of all forms of forced and compulsory labour.

- Principle 5: Effective abolition of child labour.

- Principle 6: Elimination of discrimination in respect of employment and occupation.

- Principle 7: Support a precautionary approach to environmental challenges.

- Principle 8: Undertake initiatives to promote greater environmental responsibility.

- Principle 9: Encourage the development and diffusion of environmentally friendly technologies.

- Principle 10: Work against corruption in all its forms, including extortion and bribery.

Equator Principles

JULY 2020

- Principle 1: Review and Categorisation.

- Principle 2: Environmental and Social Assessment.

- Principle 3: Applicable Environmental and Social Standards.

- Principle 4: Environmental and Social Management System and Equator Principles Action Plan.

- Principle 5: Stakeholder Engagement.

- Principle 6: Grievance Mechanism.

- Principle 7: Independent Review.

- Principle 8: Covenants.

- Principle 9: Independent Monitoring and Reporting.

- Principle 10: Reporting and Transparency.

IFC

January 2012. Performance Standards

- PS 1: Assessment and Management of Environmental and Social Risks and Impacts.

- PS 2: Labor and Working Conditions.

- PS 3: Resource Efficiency and Pollution Prevention.

- PS 4: Community Health, Safety, and Security.

- PS 5: Land Acquisition and Involuntary Resettlement.

- PS 6: Biodiversity Conservation and Sustainable Management of Living Natural Resources.

- PS 7: Indigenous Peoples.

- PS 8: Cultural Heritage.

April 2007. General Environmental, Health and Safety Guidelines

2016-Onwards. Industry Sector Guidelines

Sustainability Reporting Standards

- Sustainability Accounting Standards Board.

- Global Reporting Initiative (GRI).

- Non Financial Reporting Directive (NFRD), Directive 2014/95/EU.

- ISO 26000.

- Greenhouse Gas (GHG) Protocol.

- Carbon Disclosure Project (CDP).

- Climate Related Financial Disclosure (Recommendations from TCFD).

- Dow Jones Sustainability Indexes (DJSI) S&P Global.

References for Sustainability Governance

Recommended Links

Sustainability Governance Development and Implementation

- Sustainable Development Goals (SDG).

- United Nations Global Compact (UNGC).

- IFC Performance Standards.

- IFC EHSE Guidelines and Industry Sector Guidelines.

- Equator Principles Resources.

- Adaptive Management USAID.

- Reporting Standards.

- Sustainability Accounting Standards Board (SASB).

- Global Reporting Initiative (GRI).

- Non Financial Reporting Directive (NFRD), Directive 2014/95/EU.

- ISO 26000 Social Responsibility.

- Greenhouse Gas (GHG) Protocol.

- Carbon Disclosure Project (CDP).

- Climate Related Financial Disclosure (Recommendations from TCFD).

- Dow Jones Sustainability Indexes (DJSI).

Sustainability Assurance

What is Sustainability Assurance?

Sustainability Assurance

Sustainability Assurance (SA) is the practice of verifying and certifying the facts in the Non-Financial Disclosure of Information about Sustainability.

- Auditing and Certifying.

- Additionally may do the Sustainability Reporting.

Objectives for Sustainability Assurance

Objectives for Sustainability Assurance

- Enhance the credibility of the company’s Sustainability Reports by using a third party that ensures that the reports provide a reasonable and balanced presentation of the actual company’s performance.

- Assess the Sustainability Governance System through an external audit by comparing what is stated and what is actually implemented and in operation.

Stakeholders in Sustainability Assurance

Project Level Stakeholders for Sustainability Assurance

- Project Sponsor who invest in equity.

- Equity Investors.

- Off-Takers who receive the product.

- Lenders who lend the funds.

- Multilateral Agencies and Export Credit Agencies who also lend funds

- Insurance Providers.

Company Level Stakeholders for Sustainability Assurance

- Shareholders.

- Customers.

- Communities.

- Lenders.

- Press / Media.

Governmental Organization Stakeholders for Sustainability Assurance

- Citizens.

- Communities.

- Press / Media.

- Non-Governmental Organizations (NGOs).

Risks for not implementing Sustainability Assurance

Potential

- Increased capital costs.

- Reduced market share.

- Not extracting the full value of sustainability governance investment efforts.

- Decreased Company/Project value.

- Reputational risks due to lack of confidence in the assurance party.

Benefits of Sustainability Assurance

Top Benefits of Sustainability Assurance

- Enhanced or Protected Reputation.

- Strengthened Stakeholders Relationships.

- Enabler to meet Social Expectations.

Verification Sustainability Assurance

Sustainability Assurance Verification Process

- Planning an Audit Program.

- External Data Gathering and Analysis.

- Site Inspections.

- Audit Procedures.

- Audit Program (Independent Assurance) Conclusion.

- Recommendations for Management.

When providing non-financial information assurance services, professional audit companies are obliged to adhere to ISAE 3000, (“Assurance engagements other than audits or reviews of historical financial information”) requirements.

Standards for Sustainability Assurance

Sustainability Assurance Standards

- AccountAbiility’s AA1000.

- International Standard on Assurance Engagements 3000 (ISAE 3000).

References for Sustainability Assurance

Recommended Links

Assurance

International Standard on Assurance Engagements 3000 (ISAE 3000).

Reporting

Sustainability Accounting Standards Board (SASB).

Global Reporting Initiative (GRI).

Non Financial Reporting Directive (NFRD), Directive 2014/95/EU.

ISO 26000 Social Responsibility.

Greenhouse Gas (GHG) Protocol.

Carbon Disclosure Project (CDP).

Climate Related Financial Disclosure (Recommendations from TCFD).